Insurance FAQs...

How Much Life Insurance Do I Need?

Determining the right coverage amount depends on factors like your income, debts, and future expenses (e.g., education costs for children). Consider a policy that adequately protects your loved ones. (Pls check this out for a quick estimation Click Here)

What Is a Life Insurance Premium?

A premium is the amount you pay to keep your life insurance policy active. It can be paid monthly, annually, or in other intervals. Premiums vary based on factors like age, health, and coverage type.

What Happens If My Policy Lapses?

If you miss premium payments and your policy lapses, you lose coverage. Some policies have a grace period during which you can make late payments. Be aware of this to avoid gaps in coverage.

Why Should I Buy Life Insurance When I’m Young?

Buying life insurance early has benefits: lower premiums due to youth and better health, and the ability to lock in coverage. Plus, it provides financial security for your loved ones.

Term vs. Permanent (Whole): Which Is Better?

Term life insurance provides coverage for a specific period (e.g., 10, 20, or 30 years). Permanent life insurance lasts your entire life and accumulates cash value. Choose based on your needs.

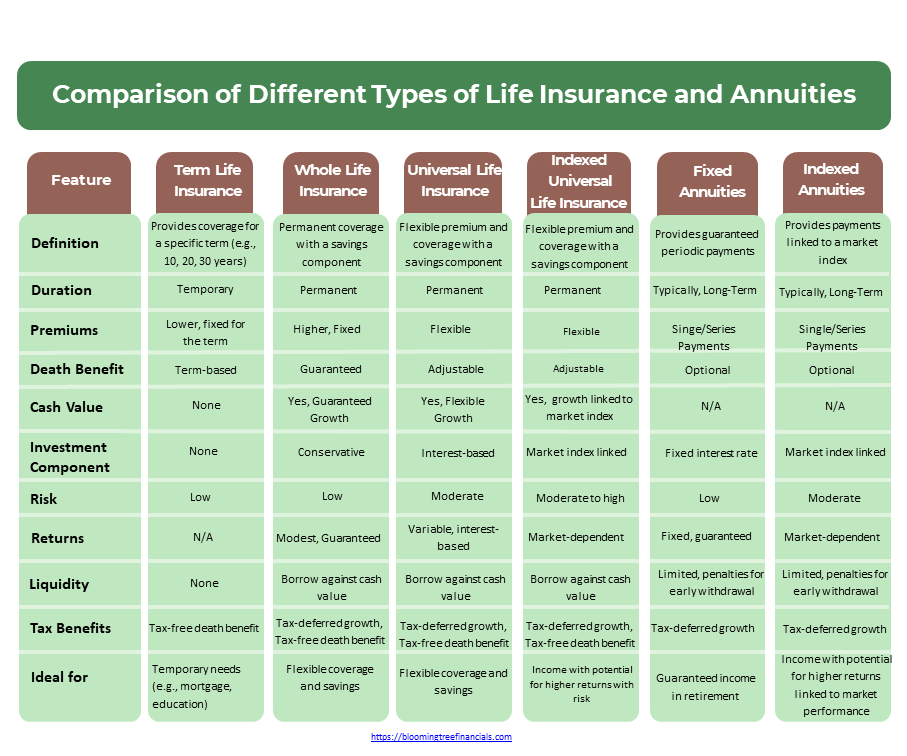

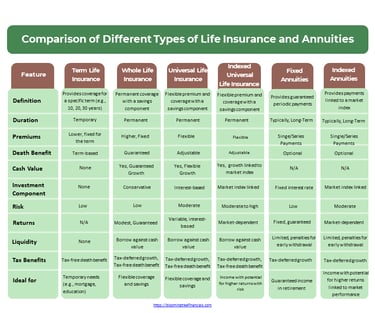

The following table provides a quick glimpse of the major features and differences between the various types of insurance and annuities.

What Is the Difference Between Whole Life and Universal Life?

Whole life insurance offers fixed premiums and guaranteed death benefits. Universal life insurance is more flexible, allowing adjustments to premiums and coverage.

Can I Convert Term Life Insurance to Permanent?

Yes, some term policies allow conversion to permanent coverage without a medical exam. It’s a useful option if you want lifelong protection.

What Riders Can I Add to My Policy?

· Riders in a term life insurance policy are additional provisions that can be added to the basic policy to enhance or customize the coverage. Here are some common riders:

Accidental Death Benefit Rider: Provides an additional death benefit if the insured dies as a result of an accident.

Waiver of Premium Rider: Waives the policyholder's premium payments if they become totally disabled and are unable to work.

Critical Illness Rider: Pays a lump sum benefit if the insured is diagnosed with a critical illness such as cancer, heart attack, or stroke.

Accelerated Death Benefit Rider: Allows the policyholder to receive a portion of the death benefit if they are diagnosed with a terminal illness.

Child Term Rider: Provides a death benefit if a child of the insured dies.

Return of Premium Rider: Refunds the premiums paid if the insured outlives the term of the policy.

Long-Term Care Rider: Provides benefits if the insured requires long-term care services.

· Riders in permanent or whole life insurance policies are additional features that can be added to enhance or customize the coverage. Here are some common riders which are offered in addition to the ones mentioned above:

1. Guaranteed Insurability Rider: Allows the policyholder to purchase additional insurance at specified intervals without undergoing a medical exam.

2. Disability Income Rider: Provides a monthly income if the policyholder becomes disabled and is unable to work.

3. Spouse Insurance Rider: Provides term life insurance coverage for the policyholder's spouse.

4. Cost of Living Rider: Increases the death benefit to keep pace with inflation, typically tied to the Consumer Price Index (CPI).

These riders can offer additional financial protection and flexibility, but they usually come at an extra cost. It's important to carefully consider which riders are necessary based on individual needs and circumstances.

Can I Have Multiple Life Insurance Policies?

Yes, you can have multiple life insurance policies. People often consider additional coverage as their needs change (e.g., marriage, children, mortgage). It’s essential to assess your overall coverage requirements and budget.

Is it possible to take life insurance for a minor ?

Yes, it is possible to take out life insurance for a minor. Here are some key points to consider:

Types of Life Insurance for Minors:

1. Child Life Insurance Policies:

Description: These are whole life insurance policies specifically designed for children. They provide lifelong coverage as long as premiums are paid.

Cash Value: These policies accumulate cash value over time, which can be borrowed against or withdrawn in the future.

Guaranteed Insurability: Some policies offer a guaranteed insurability rider, allowing the child to purchase additional coverage in the future without undergoing a medical exam.

2. Rider on a Parent’s Policy:

Description: Many life insurance companies offer the option to add a child rider to a parent's life insurance policy. This rider provides a smaller amount of coverage for the child.

Cost-Effective: Adding a rider is usually less expensive than purchasing a separate policy for the child.

Convertible: Some riders can be converted into a permanent policy when the child reaches adulthood.